Since January 2020, the S&P 500 has delivered a total return of 78.6%. But one standout stock has nearly doubled the market - over the past five years, Curtiss-Wright has surged 145% to $355 per share. Its momentum hasn’t stopped as it’s also gained 28.7% in the last six months thanks to its solid quarterly results, beating the S&P by 24.5%.

Following the strength, is CW a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Curtiss-Wright Spark Debate?

Formed from a merger of 12 companies, Curtiss-Wright (NYSE:CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

Two Things to Like:

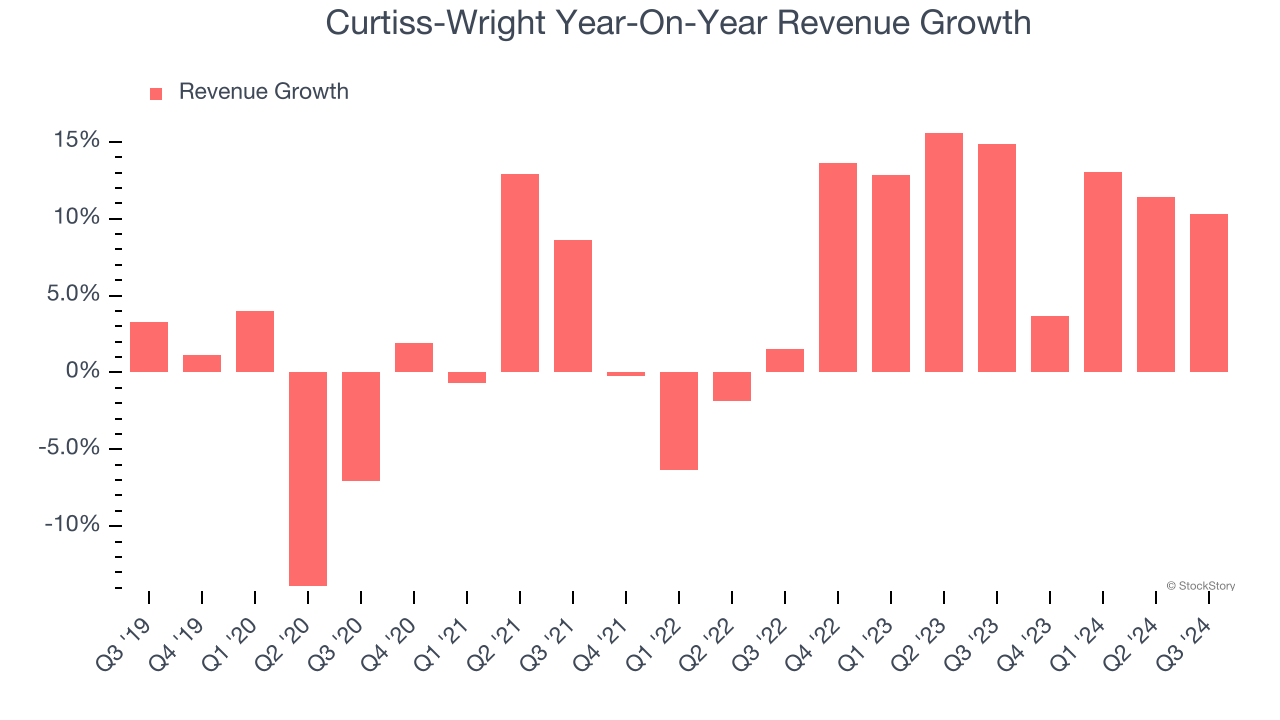

1. Skyrocketing Revenue Shows Strong Momentum

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Curtiss-Wright’s annualized revenue growth of 11.8% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

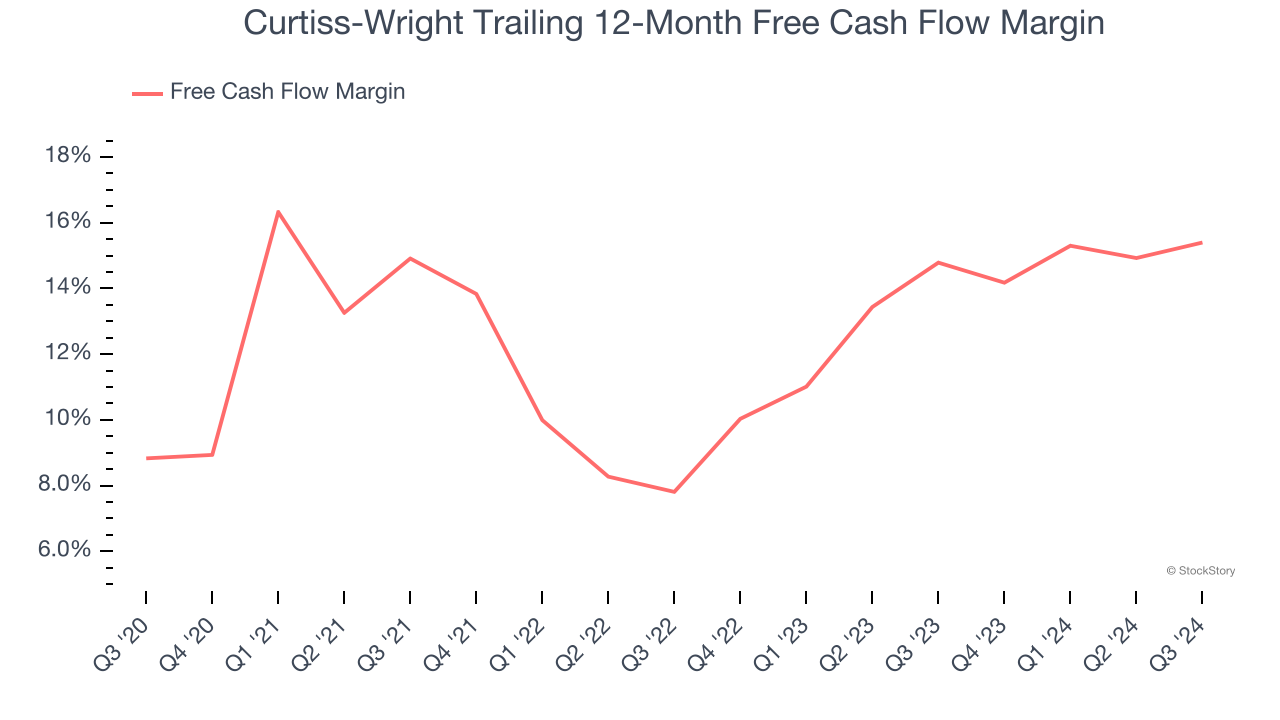

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Curtiss-Wright’s margin expanded by 6.6 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose by more than its operating profitability. Curtiss-Wright’s free cash flow margin for the trailing 12 months was 15.4%.

One Reason to be Careful:

Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Curtiss-Wright’s revenue to rise by 3.7%, a deceleration versus its 11.8% annualized growth for the past two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Final Judgment

Curtiss-Wright’s positive characteristics outweigh the negatives, and with its shares outperforming the market lately, the stock trades at 30.5× forward price-to-earnings (or $355 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Curtiss-Wright

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.