As the Q2 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the leisure facilities industry, including Sphere Entertainment (NYSE:SPHR) and its peers.

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

The 11 leisure facilities stocks we track reported a mixed Q2. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 1.4% below.

While some leisure facilities stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.2% since the latest earnings results.

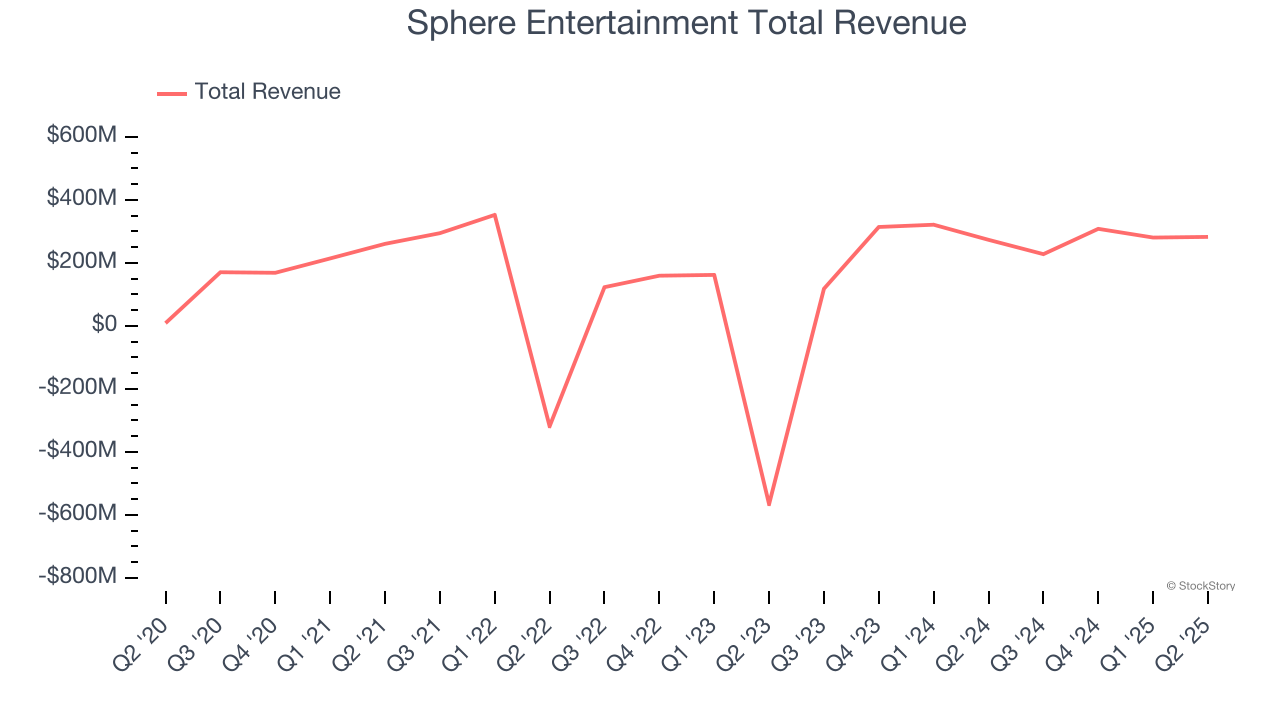

Sphere Entertainment (NYSE:SPHR)

Famous for its viral Las Vegas Sphere venue, Sphere Entertainment (NYSE:SPHR) hosts live entertainment events and distributes content across various media platforms.

Sphere Entertainment reported revenues of $282.7 million, up 3.4% year on year. This print fell short of analysts’ expectations by 7.4%. Overall, it was a slower quarter for the company with a significant miss of analysts’ revenue and EBITDA estimates.

Executive Chairman and CEO James L. Dolan said, “We continue to execute our strategic priorities to drive long-term profitable growth for our Sphere business. At the same time, we have been making progress with our expansion plans and remain confident in the global opportunity ahead.”

Sphere Entertainment delivered the weakest performance against analyst estimates of the whole group. Interestingly, the stock is up 67.5% since reporting and currently trades at $67.48.

Read our full report on Sphere Entertainment here, it’s free for active Edge members.

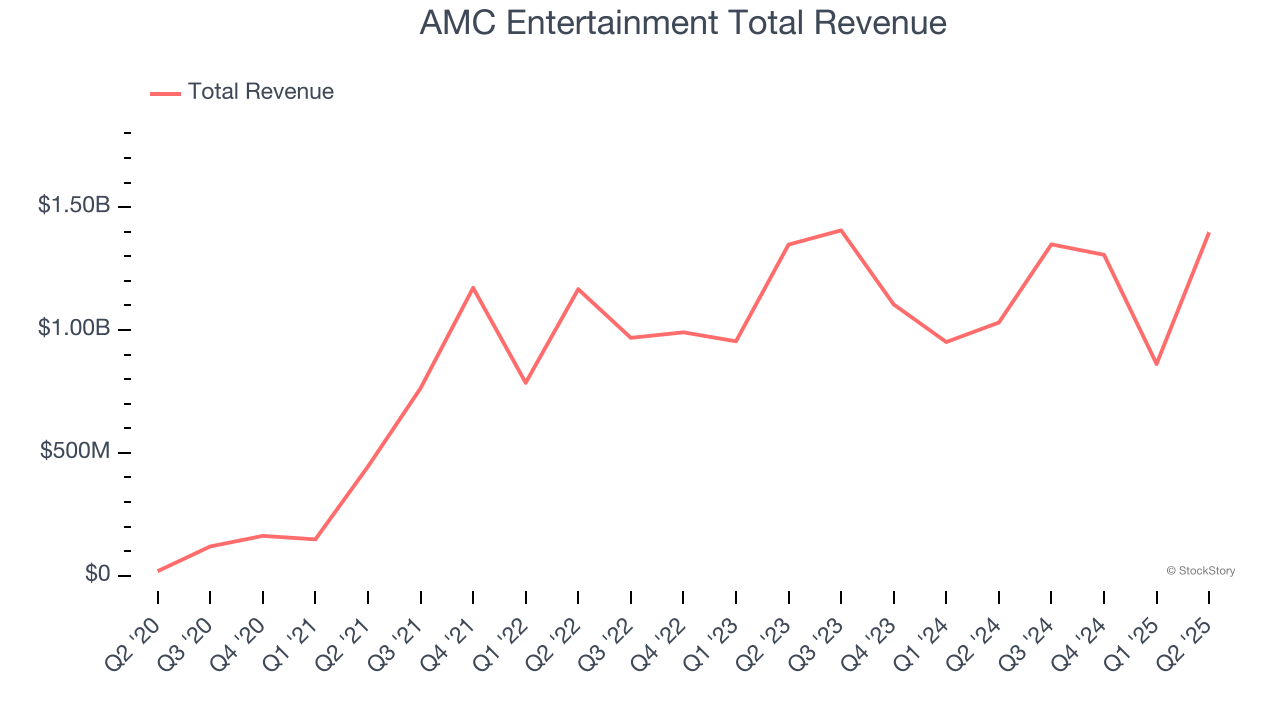

Best Q2: AMC Entertainment (NYSE:AMC)

With a profile that was raised due to meme stock mania beginning in 2021, AMC Entertainment (NYSE:AMC) operates movie theaters primarily in the US and Europe.

AMC Entertainment reported revenues of $1.40 billion, up 35.6% year on year, outperforming analysts’ expectations by 3.1%. The business had a stunning quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

AMC Entertainment achieved the fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 8% since reporting. It currently trades at $2.70.

Is now the time to buy AMC Entertainment? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: Dave & Buster's (NASDAQ:PLAY)

Founded by a former game parlor and bar operator, Dave & Buster’s (NASDAQ:PLAY) operates a chain of arcades providing immersive entertainment experiences.

Dave & Buster's reported revenues of $557.4 million, flat year on year, falling short of analysts’ expectations by 0.9%. It was a softer quarter as it posted a significant miss of analysts’ adjusted operating income and EPS estimates.

As expected, the stock is down 27.4% since the results and currently trades at $17.58.

Read our full analysis of Dave & Buster’s results here.

Vail Resorts (NYSE:MTN)

Founded by two Aspen, Colorado ski patrol guides, Vail Resorts (NYSE:MTN) is a mountain resort company offering luxury experiences in over 30 locations across the globe.

Vail Resorts reported revenues of $271.3 million, up 2.2% year on year. This result came in 0.5% below analysts' expectations. Overall, it was a slower quarter as it also recorded a significant miss of analysts’ EPS estimates and .

The stock is up 3.1% since reporting and currently trades at $152.65.

Read our full, actionable report on Vail Resorts here, it’s free for active Edge members.

Xponential Fitness (NYSE:XPOF)

Owner of CycleBar, Rumble, and Club Pilates, Xponential Fitness (NYSE:XPOF) is a boutique fitness brand offering diverse and specialized exercise experiences.

Xponential Fitness reported revenues of $76.21 million, flat year on year. This print missed analysts’ expectations by 1.5%. It was a softer quarter as it also produced full-year revenue guidance missing analysts’ expectations significantly and full-year EBITDA guidance missing analysts’ expectations significantly.

The stock is down 27.4% since reporting and currently trades at $6.98.

Read our full, actionable report on Xponential Fitness here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.