As the Q4 earnings season wraps, let’s dig into this quarter’s best and worst performers in the gas and liquid handling industry, including ITT (NYSE:ITT) and its peers.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 12 gas and liquid handling stocks we track reported a slower Q4. As a group, revenues missed analysts’ consensus estimates by 1%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.7% since the latest earnings results.

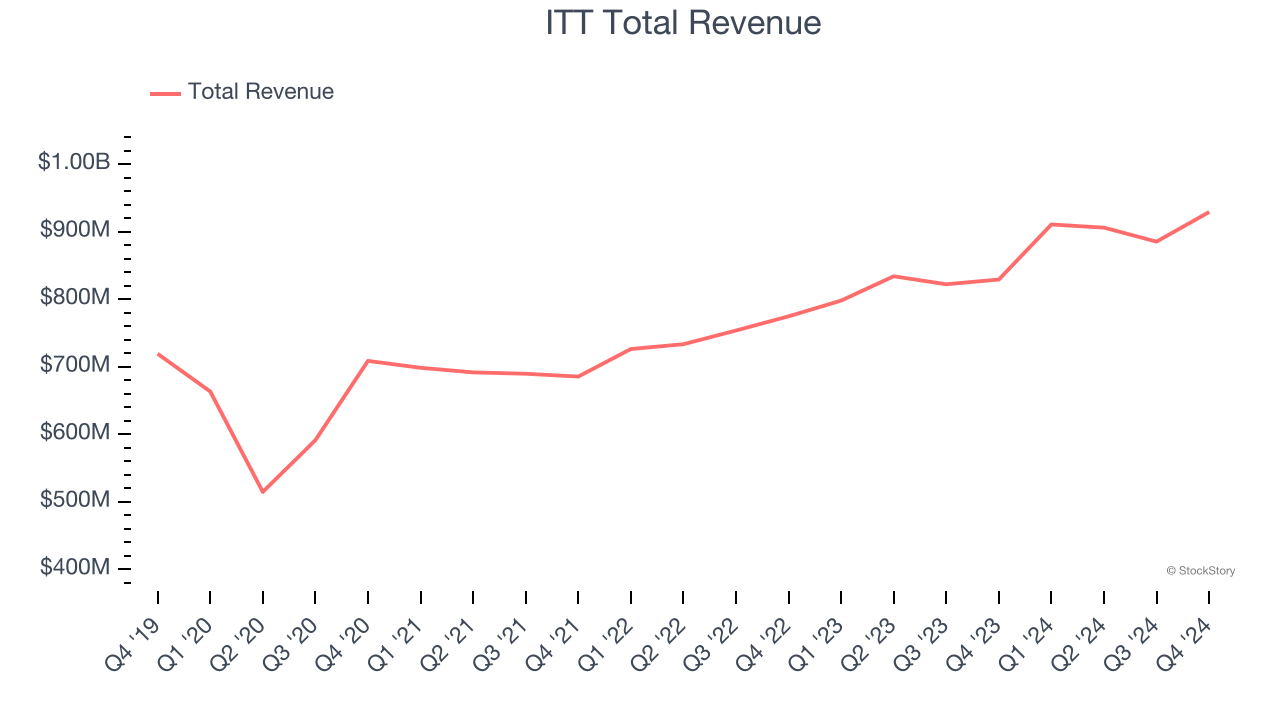

ITT (NYSE:ITT)

Playing a crucial role in the development of the first transatlantic television transmission in 1956, ITT (NYSE:ITT) provides motion and fluid handling equipment for various industries

ITT reported revenues of $929 million, up 12% year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with full-year EPS guidance missing analysts’ expectations and a slight miss of analysts’ adjusted operating income estimates.

“In 2024, our teams delivered on our commitments once again. We grew revenues 11% in total, 7% organically, with strength across all segments. ” said Luca Savi, ITT’s Chief Executive Officer and President.

The stock is down 10.4% since reporting and currently trades at $134.24.

Is now the time to buy ITT? Access our full analysis of the earnings results here, it’s free.

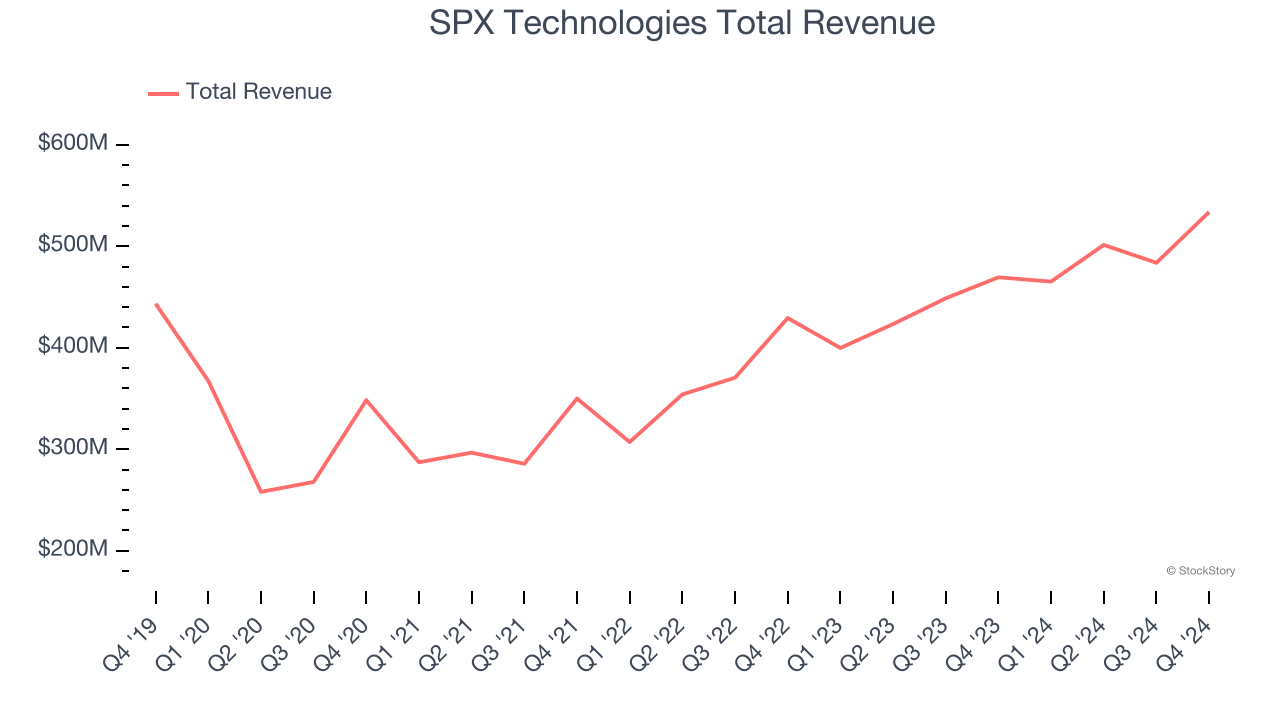

Best Q4: SPX Technologies (NYSE:SPXC)

SPX Technologies (NYSE:SPXC) is an industrial conglomerate catering to the energy, manufacturing, automotive, and aerospace sectors.

SPX Technologies reported revenues of $533.7 million, up 13.7% year on year, in line with analysts’ expectations. The business had a very strong quarter with an impressive beat of analysts’ EBITDA and organic revenue estimates.

SPX Technologies delivered the fastest revenue growth among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $137.77.

Is now the time to buy SPX Technologies? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Graco (NYSE:GGG)

Founded in 1926, Graco (NYSE:GGG) is an industrial company specializing in the development and manufacturing of fluid-handling systems and products.

Graco reported revenues of $548.7 million, down 3.2% year on year, falling short of analysts’ expectations by 1.4%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 2.9% since the results and currently trades at $83.51.

Read our full analysis of Graco’s results here.

Standex (NYSE:SXI)

Holding over 500 patents globally, Standex (NYSE:SXI) is a manufacturer and distributor of industrial components for various sectors.

Standex reported revenues of $189.8 million, up 6.4% year on year. This print beat analysts’ expectations by 0.5%. Aside from that, it was a satisfactory quarter as it also produced a solid beat of analysts’ EPS estimates but a miss of analysts’ EBITDA estimates.

The stock is down 3.4% since reporting and currently trades at $179.92.

Read our full, actionable report on Standex here, it’s free.

Helios (NYSE:HLIO)

Founded on the principle of treating others as one wants to be treated, Helios (NYSE:HLIO) designs, manufactures, and sells motion and electronic control components for various sectors.

Helios reported revenues of $179.5 million, down 7.2% year on year. This number topped analysts’ expectations by 1.3%. However, it was a slower quarter as it produced full-year EBITDA guidance missing analysts’ expectations.

Helios achieved the biggest analyst estimates beat but had the slowest revenue growth and slowest revenue growth among its peers. The stock is down 6.5% since reporting and currently trades at $36.32.

Read our full, actionable report on Helios here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.