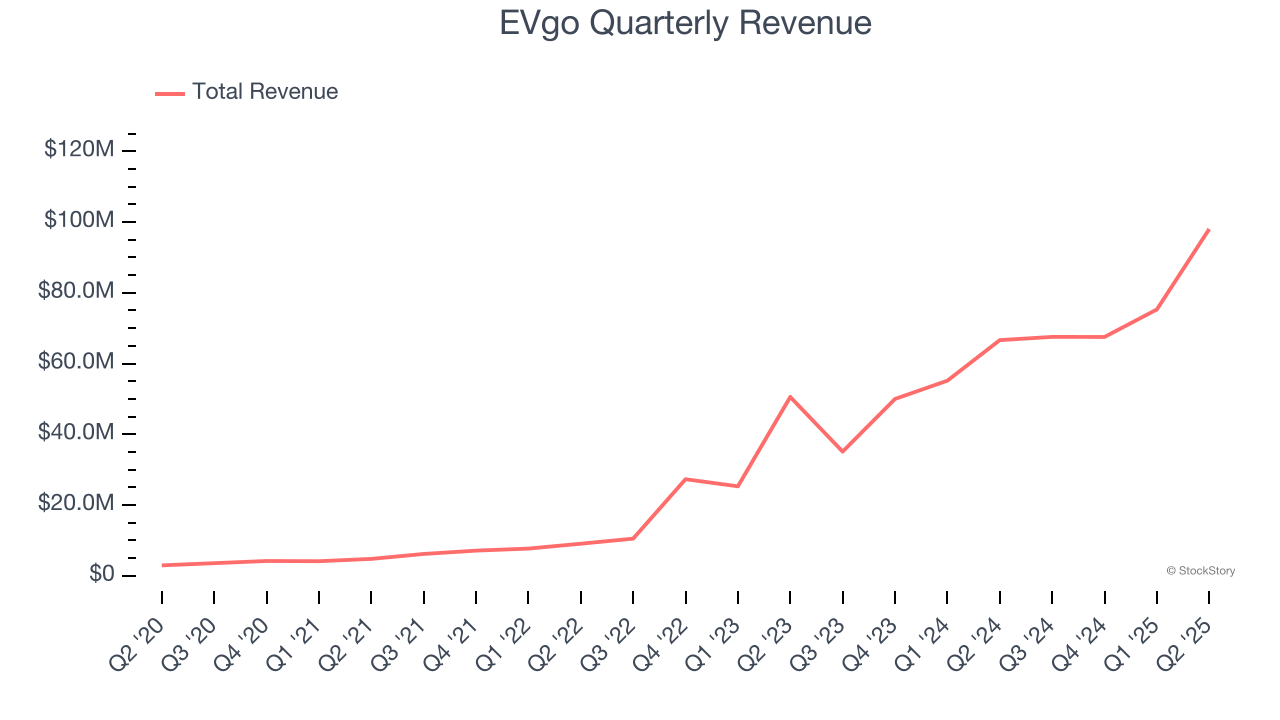

Electric vehicle charging company EVgo (NASDAQ:EVGO) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 47.2% year on year to $98.03 million. The company’s full-year revenue guidance of $365 million at the midpoint came in 3.4% above analysts’ estimates. Its GAAP loss of $0.10 per share was in line with analysts’ consensus estimates.

Is now the time to buy EVgo? Find out by accessing our full research report, it’s free.

EVgo (EVGO) Q2 CY2025 Highlights:

- Revenue: $98.03 million vs analyst estimates of $84.74 million (47.2% year-on-year growth, 15.7% beat)

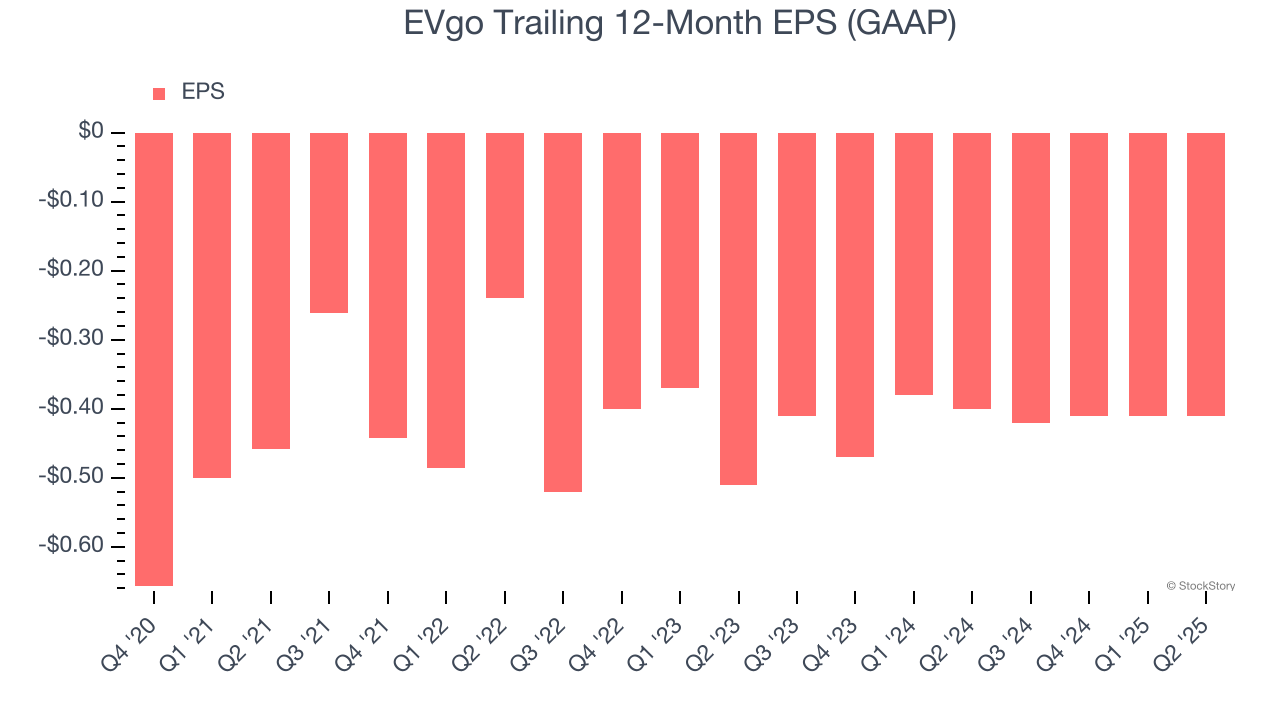

- EPS (GAAP): -$0.10 vs analyst estimates of -$0.10 (in line)

- Adjusted EBITDA: -$1.93 million vs analyst estimates of -$1.47 million (-2% margin, relatively in line)

- The company lifted its revenue guidance for the full year to $365 million at the midpoint from $360 million, a 1.4% increase

- EBITDA guidance for the full year is $2.5 million at the midpoint, above analyst estimates of $1.81 million

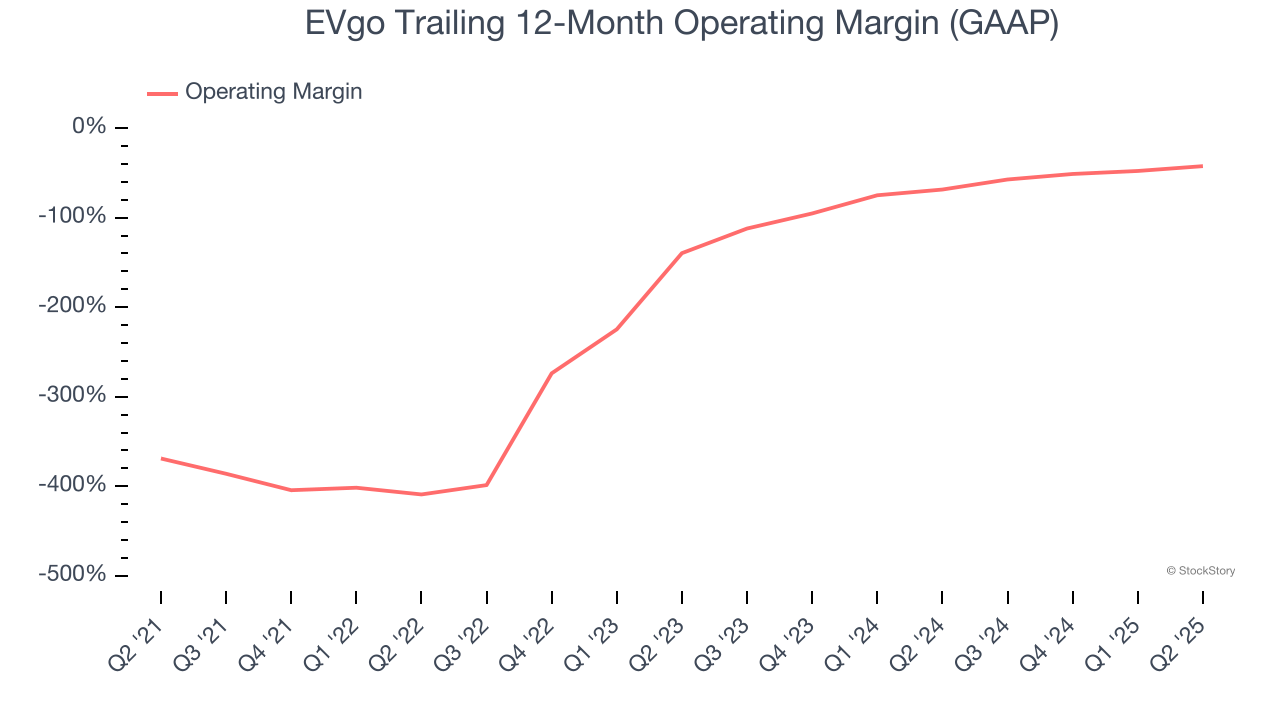

- Operating Margin: -31.4%, up from -48.6% in the same quarter last year

- Free Cash Flow was -$12.11 million compared to -$16.64 million in the same quarter last year

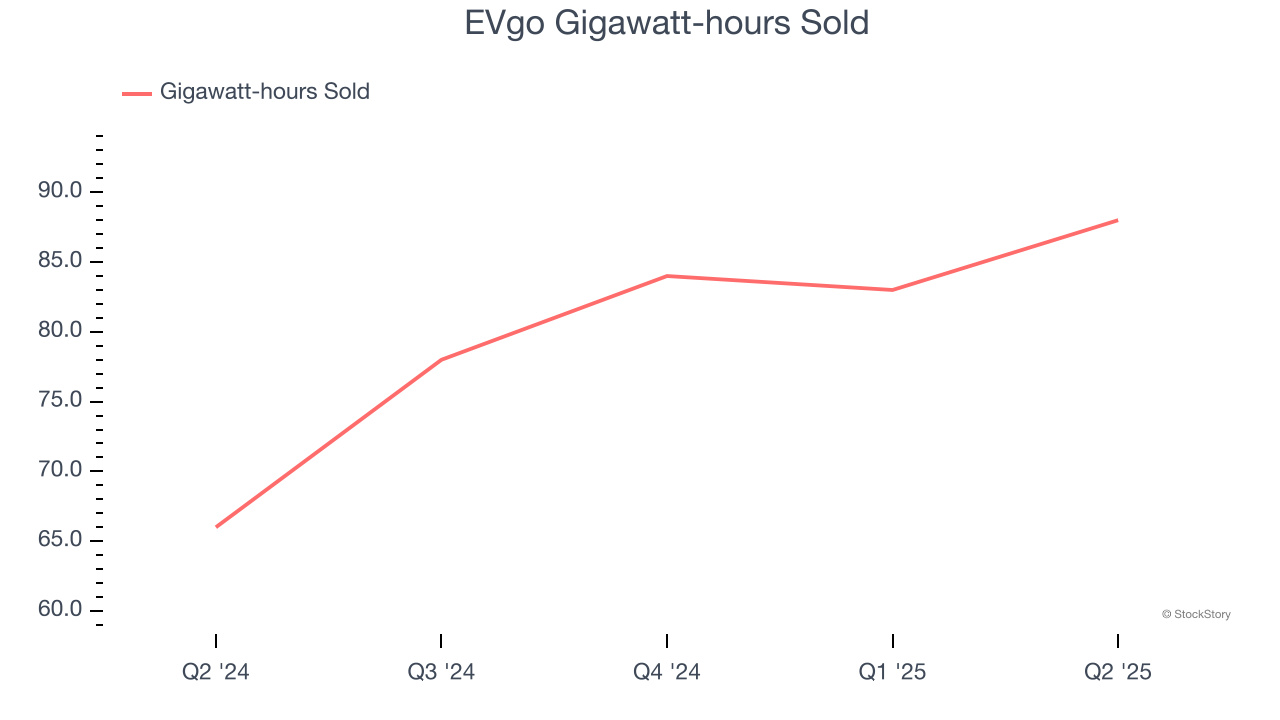

- Gigawatt-hours Sold: 88, up 22 year on year

- Market Capitalization: $473.6 million

“EVgo delivered another record quarter powered by strong operational performance, improved operating efficiencies and focused execution on our financial initiatives,” said Badar Khan, EVgo’s CEO.

Company Overview

Created through a settlement between NRG Energy and the California Public Utilities Commission, EVgo (NASDAQ:EVGO) is a provider of electric vehicle charging solutions, operating fast charging stations across the United States.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, EVgo’s 83.9% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. EVgo’s annualized revenue growth of 64.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand. EVgo recent performance stands out, especially when considering many similar Renewable Energy businesses faced declining sales because of cyclical headwinds.

We can dig further into the company’s revenue dynamics by analyzing its number of gigawatt-hours sold, which reached 88 in the latest quarter. Over the last two years, EVgo’s gigawatt-hours sold averaged 33.3% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, EVgo reported magnificent year-on-year revenue growth of 47.2%, and its $98.03 million of revenue beat Wall Street’s estimates by 15.7%.

Looking ahead, sell-side analysts expect revenue to grow 28% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and indicates the market is forecasting success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

EVgo’s high expenses have contributed to an average operating margin of negative 91.2% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, EVgo’s operating margin rose over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

This quarter, EVgo generated a negative 31.4% operating margin.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although EVgo’s full-year earnings are still negative, it reduced its losses and improved its EPS by 19.2% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For EVgo, its two-year annual EPS growth of 10.3% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q2, EVgo reported EPS at negative $0.10, in line with the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast EVgo’s full-year EPS of negative $0.41 will reach break even.

Key Takeaways from EVgo’s Q2 Results

We were impressed by how significantly EVgo blew past analysts’ revenue expectations this quarter. We were also glad its full-year revenue and EBITDA guidance trumped Wall Street’s estimates. On the other hand, its EBITDA missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 11.7% to $3.95 immediately after reporting.

Indeed, EVgo had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.