Dental and medical products company Henry Schein (NASDAQ:HSIC) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 3.3% year on year to $3.24 billion. Its non-GAAP profit of $1.10 per share was 7.6% below analysts’ consensus estimates.

Is now the time to buy Henry Schein? Find out by accessing our full research report, it’s free.

Henry Schein (HSIC) Q2 CY2025 Highlights:

- Revenue: $3.24 billion vs analyst estimates of $3.23 billion (3.3% year-on-year growth, in line)

- Adjusted EPS: $1.10 vs analyst expectations of $1.19 (7.6% miss)

- Adjusted EBITDA: $256 million vs analyst estimates of $271.4 million (7.9% margin, 5.7% miss)

- Management reiterated its full-year Adjusted EPS guidance of $4.87 at the midpoint

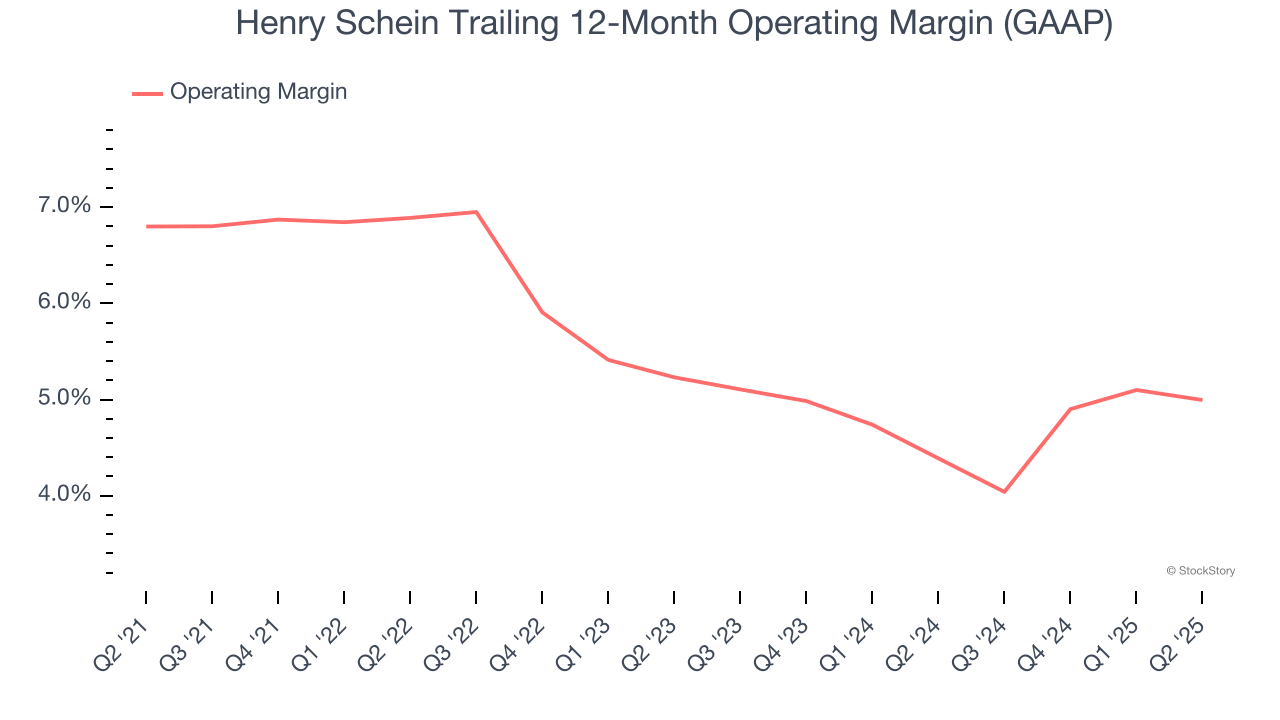

- Operating Margin: 4.7%, in line with the same quarter last year

- Free Cash Flow Margin: 2.7%, down from 8.3% in the same quarter last year

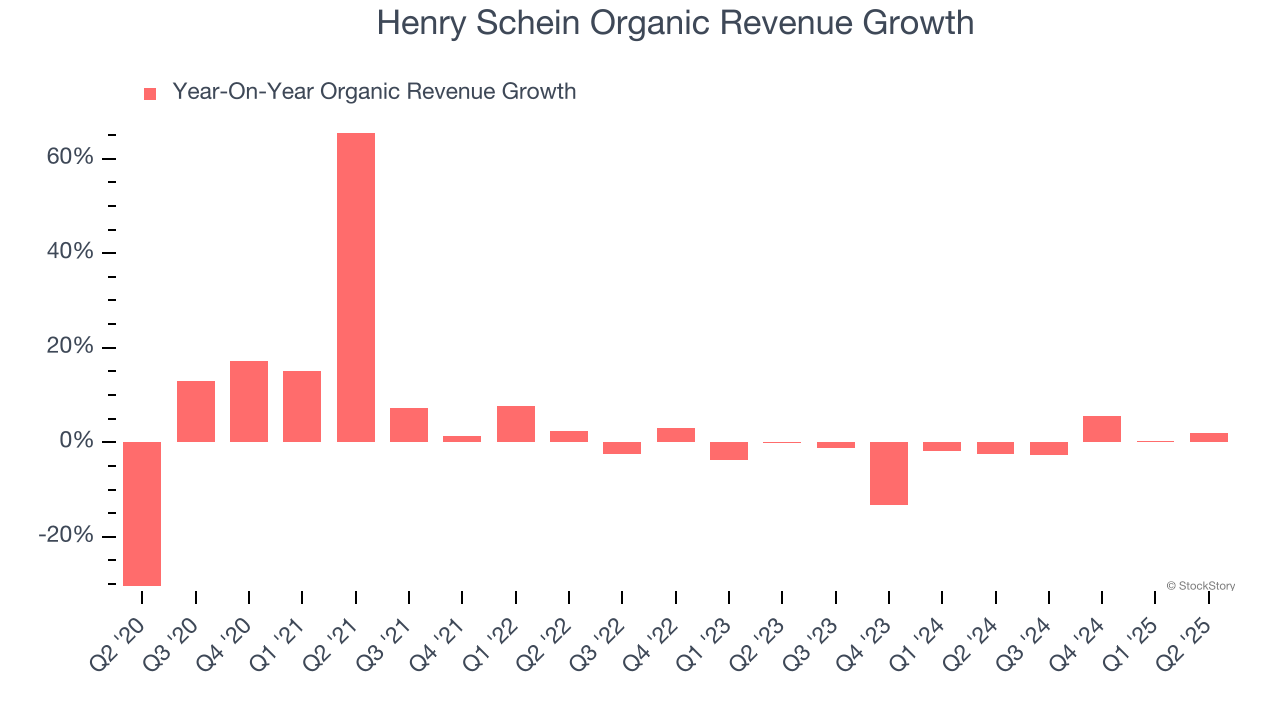

- Organic Revenue rose 1.9% year on year (-2.4% in the same quarter last year)

- Market Capitalization: $8.52 billion

“We had good sales growth in our Global Distribution Group this quarter while experiencing lower margins in the U.S. versus the prior year primarily resulting from lower glove pricing as well as time-limited targeted sales initiatives. We are pleased with the results from these initiatives and have returned to normal levels of promotional activity. Our Specialty Products and Technology Groups continued to deliver strong results, driven primarily by sales from innovative products and solutions, and cost efficiencies,” said Stanley M. Bergman, Chairman of the Board and Chief Executive Officer of Henry Schein.

Company Overview

With a vast inventory of over 300,000 products stocked in distribution centers spanning more than 5.3 million square feet worldwide, Henry Schein (NASDAQ:HSIC) is a global distributor of healthcare products and services primarily to dental practices, medical offices, and other healthcare facilities.

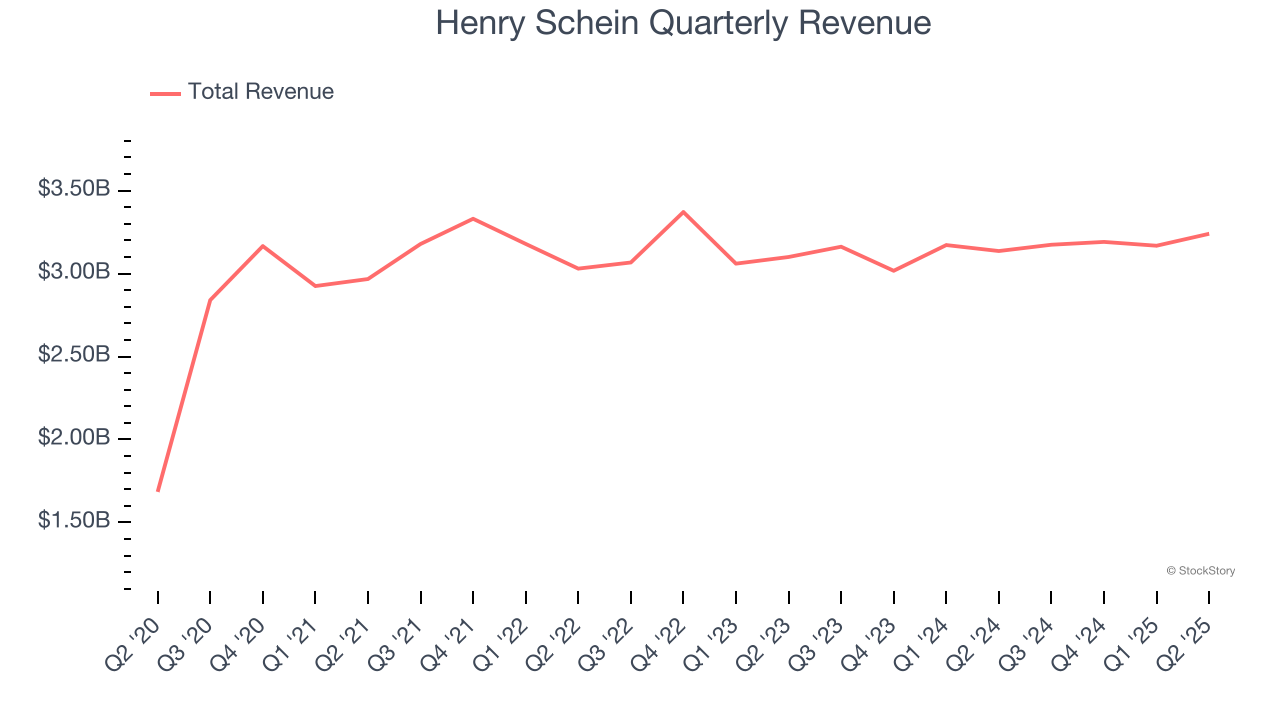

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Henry Schein’s sales grew at a mediocre 6.6% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a rough starting point for our analysis.

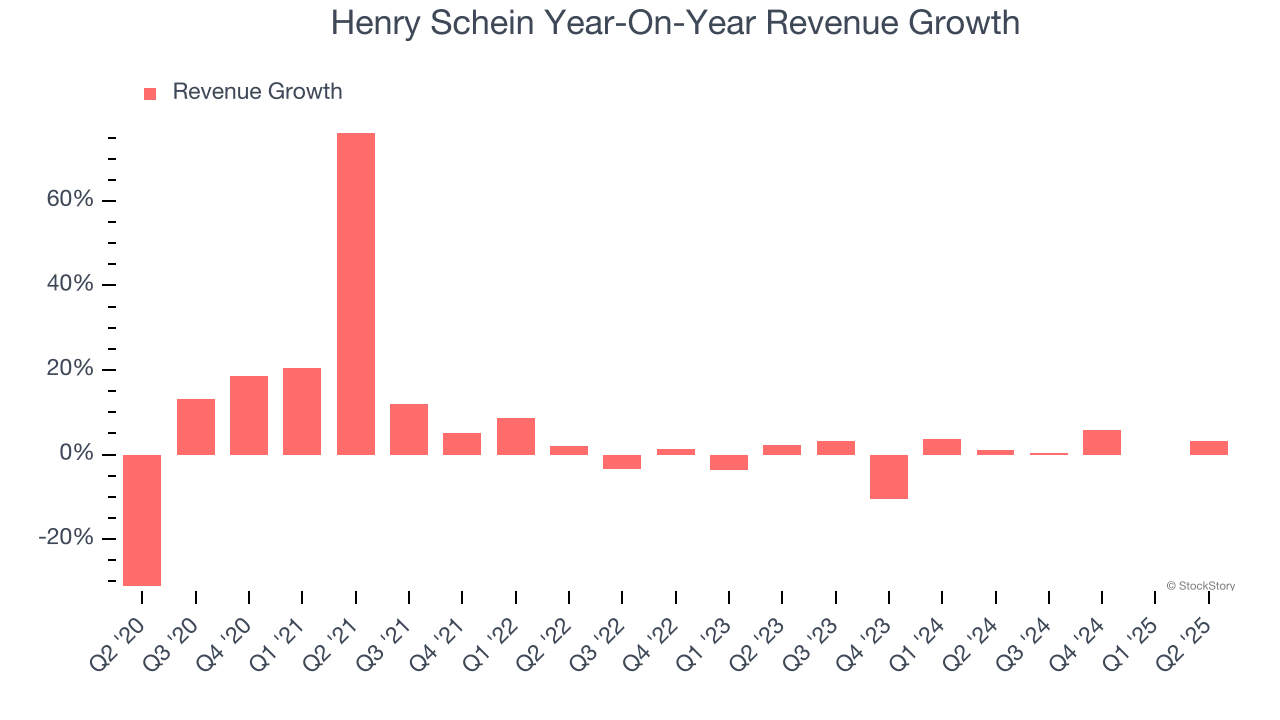

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Henry Schein’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Henry Schein’s organic revenue averaged 1.7% year-on-year declines. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Henry Schein grew its revenue by 3.3% year on year, and its $3.24 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Henry Schein was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.7% was weak for a healthcare business.

Looking at the trend in its profitability, Henry Schein’s operating margin decreased by 1.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Henry Schein’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Henry Schein generated an operating margin profit margin of 4.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

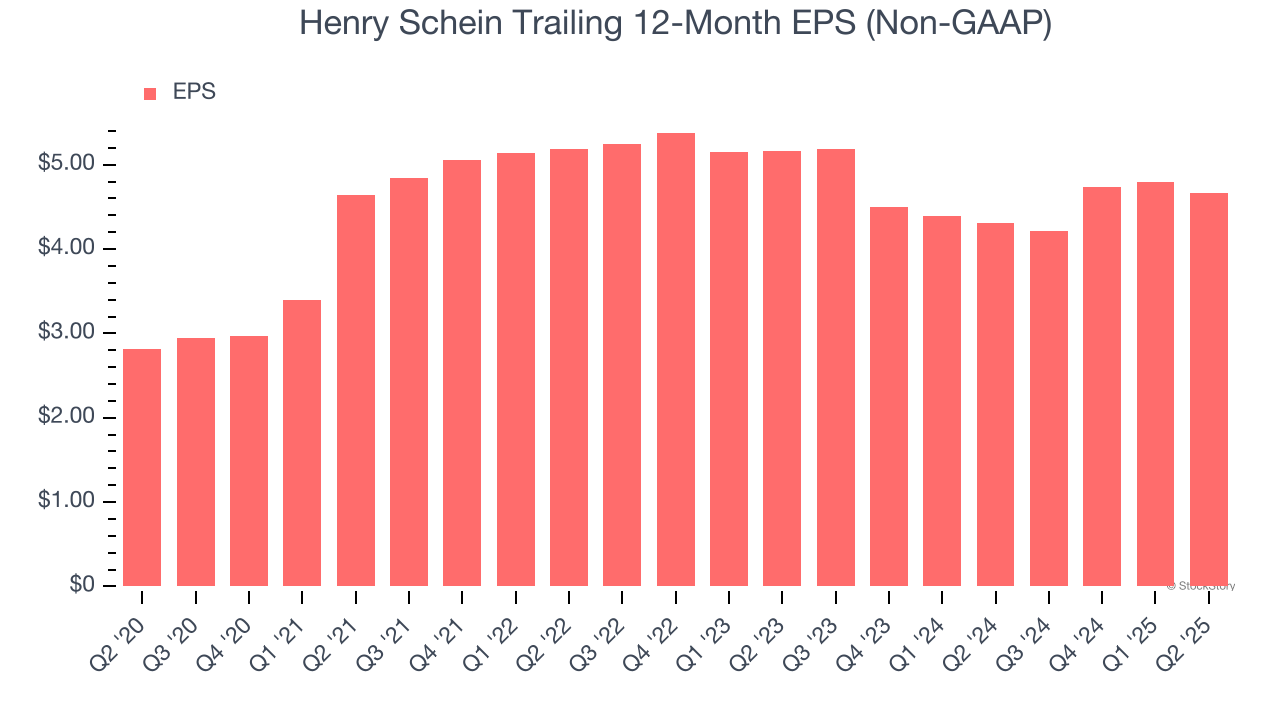

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Henry Schein’s EPS grew at a remarkable 10.6% compounded annual growth rate over the last five years, higher than its 6.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

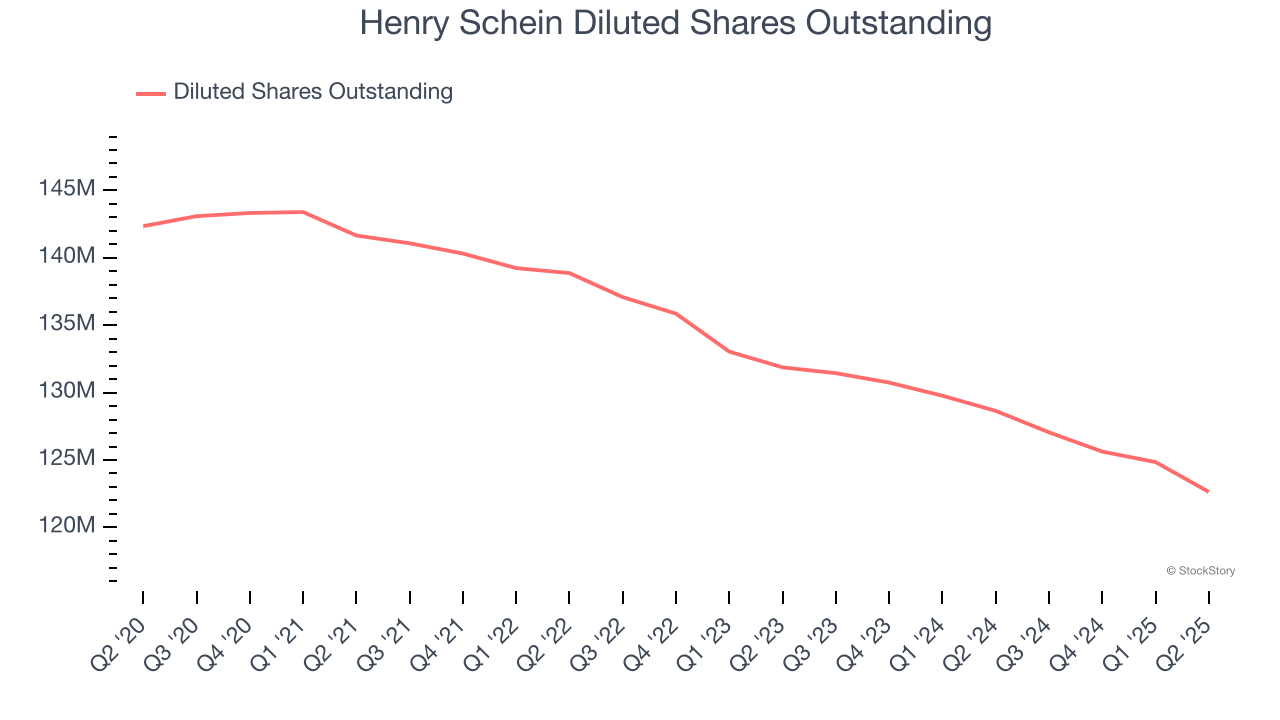

Diving into the nuances of Henry Schein’s earnings can give us a better understanding of its performance. A five-year view shows that Henry Schein has repurchased its stock, shrinking its share count by 13.8%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q2, Henry Schein reported adjusted EPS at $1.10, down from $1.23 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Henry Schein’s full-year EPS of $4.66 to grow 8.2%.

Key Takeaways from Henry Schein’s Q2 Results

We struggled to find many positives in these results. Overall, this was a weaker quarter. The stock traded down 4.8% to $66.76 immediately after reporting.

The latest quarter from Henry Schein’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.